RBI holds repo rate as inflation pressure persists; imposes I-CRR to drain liquidity

The spike in vegetable prices, uncertainties on domestic food price outlook due to sudden weather events and firm crude oil prices prompted the six-member Monetary Policy Committee (MPC) to unanimously vote to keep the policy repo rate on hold even as the Reserve Bank of India revised its FY24 inflation forecast upwards.

The central bank also prescribed maintenance of incremental cash reserve ratio (I-CRR) by banks to drain out excess liquidity from the banking system.

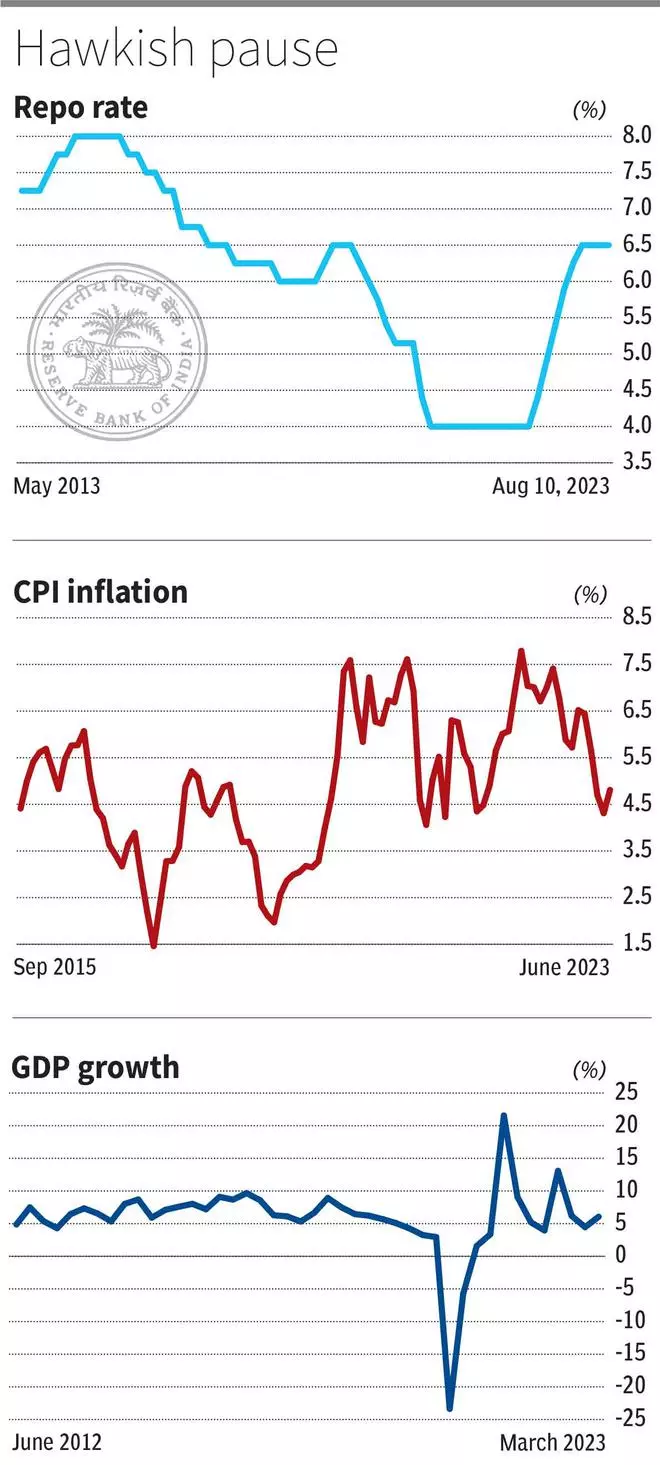

Repo rate at 6.5%

The MPC’s decision to maintain the repo rate at 6.50 per cent for the third time on the trot in as many meetings was widely expected. Repo rate is the interest rate at which banks borrow funds from RBI to overcome short-term liquidity mismatches.

The committee voted by a majority of five to one to remain focussed on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.

Inflation forecast revised

The RBI revised its forecast for consumer price index-based (retail) inflation for FY24 upwards from 5.1 per cent to 5.4 per cent due to persisting inflationary risks. It maintained real GDP growth projection for FY24 at 6.5 per cent.

“I reiterate our commitment to align CPI inflation to the 4 per cent target on a durable basis. We do look through idiosyncratic shocks, but if such idiosyncrasies show signs of persistence, we have to act,” Das said. Market players interpreted this statement as an indication of the central bank’s hawkish tilt.

The Governor said the frequent incidences of recurring food price shocks pose a risk to anchoring of inflation expectations, which has been underway since September 2022.

“The role of continued and timely supply side interventions assumes criticality in limiting the severity and duration of such shocks. In such circumstances, it is necessary to be watchful of the emerging trends and risks to price stability.

“We have to stand in readiness to go beyond keeping Arjuna’s eye to deploying policy instruments, if necessary,” he said, adding that there has been good progress in sustaining India’s growth momentum.

Das emphasised that while inflation has moderated, the job is still not done. Inflationary risks persist amidst volatile international food and energy prices, lingering geopolitical tensions and weather-related uncertainties, he added.

Headline inflation, after reaching a low of 4.3 per cent in May 2023, rose in June and is expected to surge during July-August led by vegetable prices, per RBI’s assessment.

Given the likely short-term nature of the price shock from vegetables, monetary policy can look through high inflation prints caused by such shocks for some time, the Governor said.

“We expect the MPC to hold on policy rates in the next meeting, as it awaits a clearer picture on the inflation path. A 25-basis points rate cut in early 2024 is a conditional possibility for now,” Crisil Ratings.

Incremental CRR: ₹1-lakh crore to be drained

The RBI asked scheduled banks to maintain (with effect from the fortnight beginning August 12, 2023,) an incremental cash reserve ratio (I-CRR) of 10 per cent on the increase in their deposits between May 19 and July 28. The existing CRR (the cash parked by the banks in their specified current account maintained with RBI) remains unchanged at 4.5 per cent.

Das said this measure is intended to absorb the surplus liquidity generated by various factors such as the return of ₹2000 notes to the banking system, RBI’s surplus transfer to the government, pick up in government spending and capital inflows. The move is being seen as a warning shot to the banks after attempts by the RBI to suck out liquidity through 14-day variable rate reverse repo (VRRR) auctions have met with limited success.

With I-CRR, RBI is hoping to take out liquidity amounting to a little over ₹1-lakh crore.

Tighter liquidity conditions could imply some upward pressure on both credit and deposit rates as transmission of past rate hikes improves, Abheek Barua, Chief Economist, HDFC Bank, said.

“Deployment of policy instruments are not just in terms of rate and stance, there are other ways of dealing with it. We have done a bit with regard to the incremental CRR today.

“This was considered necessary in the background of the liquidity overhang. We considered it desirable in the interest of price stability and financial stability. It will have an impact on the inflation situation also. This is purely a temporary measure for managing the liquidity overhang,” Das said.

The Governor underscored that even after this temporary impounding, there will be adequate liquidity in the system to meet the credit needs of the economy.

The I-CRR will be reviewed on September 8or earlier to return the impounded funds to the banking system ahead of the festival season.